Assisted Living

CORONAVIRUS AND LONG TERM CARE

COVID-19’s added costs likely will lead to increases in insurance premiums and long-term care costs!

More than 18 million people have been infected by coronavirus worldwide, about a quarter of them in the United States. It is likely to be years before the costs for those who have recovered can be fully calculated, according to Reuters interviews with approximately a dozen physicians and health economists.

These experts point to the potential for billions of dollars in long-term healthcare expenses, as studies of patients with COVID-19 continue to uncover new complications associated with the disease. They say the costs stem from COVID-19’s toll on multiple organs, including heart, lung and kidney damage that likely will require costly care, such as regular scans and ultrasounds, as well as neurologic deficits that are not yet fully understood.

The added costs likely will lead to increases in insurance premiums and long-term care costs. Bruce Lee of the City University of New York Public School of Health estimated that if 20% of the U.S. population contracts the virus, the one-year post-hospitalization costs would be at least $50 billion. This is before factoring in longer-term care for lingering health problems. Without a vaccine, if 80% of the population became infected, that cost would jump to $204 billion.

“On a global level, nobody knows how many will still need checks and treatment in three months, six months, a year,” Marco Rizzi, M.D., a physician in Bergamo, Italy told Reuters. Rizzi has seen nearly 600 people with COVID-19 for follow-up. He is co-chairing a World Health Organization panel recommending long-term follow-up for patients. Even those with mild COVID-19 “may have consequences in the future,” he added.

LTC Comment: Covid-19 hit LTC when it was already down. The perfect storm of an oncoming economic catastrophe and growing long-term health care costs may finish the welfare-financed system. Will private financing markets, including home equity conversion and private LTC insurance, fill the breach?

How will you or your clients pay for their LTC costs?

Assets have lost value, LTC costs are up and likely to go higher. LTC insurance with an automatic 5% compound inflation factor WILL keep up with increasing costs and allow those insured to get the care they need where they want it, instead of relying on a Medicaid nursing home.

Don’t get caught in this long term care trap! Many people are.

Often agents sell policies for a cheaper price because they didn’t include the all-important automatic inflation on benefits. Don’t get caught in this long term care trap!

I am being approached by many people who purchased long-term care (LTC) insurance many years ago. They bought the LTC insurance from their life insurance agent, their financial planner, or their home insurance agent – not a specialist in LTC. These agents knew life or home owners insurance, but often just “dabbled” in long term care sales. Maybe they had just one company’s product to sell. Often, they sold the policies for a cheaper price because they didn’t include the all- important automatic inflation on benefits.

Long term care costs have been increasing more quickly than inflation, doubling almost every 15 years.

For example, a nursing home that charged $4500 a month 18 years ago, now charges over $10,000 a month. Costs may increase even more quickly in the future because labor costs are likely to increase. Since we have nearly full employment, employers may need to offer higher wages to attract the needed workers. We also hear talk about increasing the minimum wage to as much as $15 per hour, so costs could increase even faster.

If you have an older LTC insurance policy that doesn’t include inflation coverage, there still may be something that you can do. If you are considering investigating LTC insurance – do so with an expert. You need an expert who knows the costs, understands inflation and knows what the options are for people with these kinds of policies, so that the expert can help you determine how much of the bills you can pay yourself. That way, you don’t buy too much insurance.

I am an expert in long term care financing. I have been doing nothing but LTC planning and financing for over 25 years. I am happy to review your policy. I can help you if there are problems with your policy. I can help protect some of the money if LTC is needed and you have not prepared in advance. Many of my clients have been referred to me by their financial planner or their attorney. Learn more about me at www.thelongtermcareguy.com.

If you want to investigate how to deal with LTC, call (920) 884-3030. Let’s plan a time to investigate together.

Why Can’t I Spend my Money on Fun?

Often, retired people are afraid to spend money on fun or travel because they fear the catastrophic costs!

A recent Wall Street Journal cartoon featured a gentleman visiting his financial planner. In the cartoon, he asks the planner, “Why can’t I spend some of my money on fun now?”

Often, retired people are afraid to spend money on fun or travel because they fear the catastrophic costs they would face if one of them needs long term care (LTC). This can be a real concern, because the U.S. Department of Health and Human Services says that 70% of people who reach age 65 will need some long-term care. The great majority of us cannot afford it for long if we’re paying out of pocket.

Many people assume the insurance for LTC is prohibitively expensive. This is because they never investigated what the costs actually would be for them. I can tell you with near certainty that you need less of it than you imagine. When you finally need care, your lifestyle will change considerably. If you cannot drive there will be fewer vehicles, boats, toys, and less travel, golf, dining out, and so on. The money spent on fun (which you SHOULD do while healthy) can be redirected towards the costs of LTC.

Most people have some savings. Without touching the principle, you can spend the interest or yield it generates. Add this to the savings from your lifestyle changes, and you may find you can cover a significant portion of the costs of LTC yourself. You will only need to cover the shortfall from some other sources, like insurance, so you do not spend down all your savings and end up on Medicaid.

People investigate LTC insurance for two reasons.

- First, they do not want to go broke.

- Second, many long-term care service providers will not accept Medicaid. Nursing homes generally have to because of federal laws–but a nursing home is usually the last place you want to be. If you have the ability to pay from your cash flow and insurance, it will let you choose where and how you will be cared for. The providers will welcome you with open arms!

If you have not investigated LTC insurance, now is the time, while you are still healthy enough to get it.

It is a logical discussion and it is not appropriate for everyone. But please investigate with someone knowledgeable in planning for LTC. At The Long Term Care Guy, we have been doing only LTC planning for over 25 years. Since nearly all of our business comes to us by referral, we may even may be working with your financial planner or attorney!

Call TheLongTermCareGuy.com at (920) 884-3030 or email us for a time to investigate your situation.

Why Medicaid Long Term Care is a Bad Choice

Most assisted living facilities don’t accept Medicaid, so often Medicaid recipients needing LTC are left with only one choice—a nursing home.

Many people don’t realize that, in addition to traditional health care, Medicaid actually pays for most long-term care (LTC) in the United States. In fact, less than 40% of Medicaid dollars are used to pay for traditional health care. The small portion of Medicaid recipients (just over 20%) whose long-term care services are paid for by Medicaid use over 60% of the Medicaid budget dollars.

Most assisted living facilities don’t accept Medicaid, so often Medicaid recipients needing LTC are left with only one choice—a nursing home. This is because the federal government requires nursing homes to accept Medicaid payments if they want to accept Medicare for the rehab care they provide–and this rehab care is a major source of revenue for many nursing homes.

Wouldn’t you rather receive care, when needed, at home or in an assisted living facility rather than the nursing home? Most people would, but if you cannot afford this care – your only option might be the nursing home.

Many people mistakenly assume LTC insurance is too expensive. It can be, if it’s not chosen appropriately. Do you have a deductible on your car insurance or does it cover every last penny? Mine has a deductible, so that I pay the first part and insurance pays the expensive part.

LTC is similar. Your lifestyle will change when care is needed. You will spend less money on vehicles if you cannot drive, and spend less on golf, travel, toys, and so on. The money freed up by not spending it on these things needs to be taken into account in order to see how much care you can pay for. Then you only need enough insurance to cover the shortfall. If you have a nest egg, and do not want to use it all up, you can always take the interest it generates to help lower the insurance need even more—and never touching the principal.

Think you cannot get LTC insurance because of health? I have solutions for nearly every situation – even some for people already in care.

So, you can ignore this and hope you will not be among the 70% of us who will need care – or you can investigate options to see if this concern can be handled affordably. Your choice!

www.TheLongTermCareGuy.com Romeo Raabe is here to help, even with just advice.

Happy Holidays – How is Grandma?

How is Grandma? Are bills piling up unpaid? Is hygiene slipping? Are they not eating as well as they should, or is the house unkempt?

While your family was together at Thanksgiving, was there evidence that older family members are not taking care of themselves as well as they could be or used to?

Perhaps your loved one is not driving as much as before, or perhaps should not be driving at all. Are bills piling up unpaid? Is hygiene slipping? Are they not eating as well as they should, or is the house unkempt?

It is never easy to meet with siblings and parents to talk about how and where they will be helped with future living arrangements. Then you check into costs at senior living facilities and wonder how can this possibly work.

Hello! My name is Romeo Raabe, and I am a long-term care (LTC) planner at www.TheLongTermCareGuy.com. I help families learn how to convert homes into income to pay for LTC facilities.

I help families navigate the federal Medicaid programs that can pay for LTC. I even have ways to help protect the money for family, rather than all going toward LTC costs.

If this discussion has started, or is about to, call me at (920) 884-3030 and let’s schedule a time to visit and see if I can help you and yours. It’s never too late and you don’t know what you don’t know.

What’s it Really Like Paying for Long-Term Care

Annual cost range is $18,720 for adult day-care services to $100,375 for a private room in a nursing home!

As written by Michelle Singletary and published in the Washington Post on November 26, 2018

One of my favorite Spock quotes from the Star Trek television series is, “Live long and prosper.” Who doesn’t want a long life, right?

But what if the longevity means spending down your money for long-term care? And that’s if you’ve been prosperous and have the funds to pay a facility or home health aide to care for you.

Genworth Financial recently released its 2018 Annual Cost of Care survey and found that the annual median cost of care now ranges from $18,720 for adult day-care services to $100,375 for a private room in a nursing home.

I asked readers to share their long-term care experiences, and here’s what they had to say:

“My mother had Alzheimer’s and was in a memory unit for two years,” wrote Chris Gonzales from California. “My dad has been in assisted living for two and half years and for the last two years has needed round-the-clock care. The cost, when my mother was alive, totaled $230,000 a year. The cost to care for dad is now $170,000 a year. This is in Fort Smith, Ark. My brother and I are very lucky that our parents lived below their means, saved, and did extremely well investing their money in the market, so money has not been an issue. We are also grateful for the ladies that watch over our father and consider ourselves extremely lucky to have people we can depend on as we both live out of state.”

“I managed the care of my mother (who had Alzheimer’s disease) from 1998 through 2006,” wrote Debbie Trice of Sarasota, Fla. “Even that long ago, the cost of her care approached $100,000 annually once she had to move from an assisted-living facility to a skilled nursing facility. The actual cost of long-term care goes way beyond the monthly or daily facility charges. Personal expenses (e.g., adult diapers, toiletries, laundry, haircuts) can be significant. I saved some money by purchasing diapers from a wholesaler and toiletries from a discount store and doing mother’s laundry myself. Medications cost more for residents in long-term care, too. Some states require that all medication, including over-the-counter items like aspirin and vitamins, be specially packaged by a pharmacist in blister packs — at extra cost, of course. Staffing is a critical issue. To keep their rates competitive, many facilities limit their staffing levels to the minimum required by law. But then some patients’ needs can’t be adequately addressed. I found it necessary to hire private duty aides to supplement facility staff for a few hours each day.”

Lane Beckham of New Jersey wrote, “Four years ago my wife (then 71) suffered a fall which led to numerous complications over the next year. She has since been bedridden going from a home hospital bed to a wheelchair. She can feed herself, converse, watch television and read catalogues, but that’s about it. We’ve had a 24/7 home health care aide since April 2015 at a current cost of $215 a day or $78,475 a year. A long-term care policy kicks in $100 a day but only for 5 years of benefit days.”

“My mother died two years ago and for the last two years of her life, she had progressively worsening dementia,”

One reader wrote. “We (mainly my sister) arranged for her to be cared for at her home. The cost was running at about $85,000 a year and that was two years ago! Why? At times, she was simply too much for one person to handle, so we often needed two people to stay with her. And while we went with the better-rated agencies, we still had problems with sitters stealing, using drugs, having friends over and even taking my mother out when they needed to run errands. What a nightmare.”

David Treece, an investment adviser and financial planner based in Miami Shores, Fla., has a client with Alzheimer’s who has a Genworth long-term care insurance policy, which so far has paid out about $323,000.

“I have learned nothing will ruin a retirement plan faster than long-term care expenses,” Treece wrote. “Try having to come up with nearly a third of a million dollars like my client if you don’t have coverage. It’s just unimaginable for most people. My biggest concerns for my clients are a group I call ‘the alones.’ These are people who have no spouse, no children, no close siblings and really nobody else. They can’t even name a beneficiary let alone someone to serve as a power of attorney or health-care surrogate. This group seems to be increasing as so many people never had children, are divorced or never married, or are estranged from family. Who is even going to help them? Our society isn’t really set up for this, and I don’t see any easy solutions.”

*****

How comfortable do you feel paying for care out of pocket when your health changes?

- Have you thought that Long-Term Care insurance would not be needed?

- Do you plan on spending down to Medicaid, a welfare program and then search for a place that will accept it – and you?

If you are concerned, contact www.TheLongTermCareGuy.com at (920) 884-3030 and schedule a time to investigate with someone who understands and can help you find a way to handle this!

Who is Going to Pay for Your Funeral?

Who is Going to Pay for Your Funeral?

Asking who is going to pay for your funeral might seem like a silly question–you probably have money in savings, a vehicle, a house, even life insurance. There should be plenty of money to pay this bill, right?

The problem is, you are gone, so now who has access to your assets?

Your Power of Attorney ends at the moment of your death. How your assets will be distributed and who has authority will all be determined in the probate process in the next few months. So, who will come up with the funds now to pay for the funeral? Even life insurance does not pay out for some time once claim forms are submitted.

Just recently, I received a call from a La Crosse funeral home who wanted to know how to get in touch with the Wisconsin Funeral Trust. This is the organization that funeral directors set up to hold prepayments for funerals. The association chose to invest the funds very aggressively and now only has money to pay out 65% of what people deposited. The funeral home that called me was caring for two individuals who had passed, and the home was trying to determine how much money the trust actually has for them. They called me is because they found me in an internet search. (If you Google “funeral trust Wisconsin”, my website comes up.) They hoped I could either help them or direct them to the correct place.

This shortcoming of the state funeral trust is important to those planning ahead for their end-of-life needs. I am a long-term care planner and, as such, include protecting funds set aside for funerals as part of my work. I help people set aside funds for their funeral using a licensed trust company who specializes in just this. The company that I use for this purpose is a licensed and bonded insurance company, required by law to retain adequate funds to cover claims. There is no cost to set up such a trust and the funds deposited earn interest. These funds are available immediately at death, even before a death certificate has been produced, to pay all the bills in full.

There is another important reason to fund a funeral trust –many people need long term care in the years leading up to their death. This can cost as much as $50,000 to $90,000 per year or more. If they did not plan in advance and purchase long-term care insurance to cover these bills, they may have to apply for a welfare program called Medicaid to pay for their care. Medicaid is a payer of last resort and will only cover long-term care expenses once you have spent down everything you own (house, car, checking, savings) to under $2000. You must also cash in life insurance before Medicaid pays for long-term care. This balance is not enough to pay for a funeral.

Medicaid does allow you to set aside money for funeral expenses, but only in an irrevocable burial trust account. Setting these up for people who did not plan for long-term care expenses has become a large part of my work.

Death happens to everyone. Don’t leave the bills for this to your children. Make sure the money is there AND accessible to them when it is needed.

Long-term care happens to 70% of adults who make it to age 65. What is your plan to pay for this care when your health changes?

For answers to either of these predicaments, reach out to Romeo Raabe at www.TheLongTermCareGuy.com or call (920) 884-3030 to schedule a time to investigate solutions. There is never a cost to investigate.

Observations from a Recent Hospital Stay

Nearly every one of the CNAs at a recent hospital stay started their careers in a long-term care (LTC) facility.

Recently, I was an inpatient in a hospital after having surgery. While there, I visited with a number of nurses and CNAs (certified nursing assistants) while they were caring for me. Nearly every one of the CNAs had started their careers in a long-term care (LTC) facility. The reasons these workers moved on to a hospital setting for work is the main problem with LTC today.

Caregivers (CNAs) are in very high demand and very short supply.

LTC workers especially are underpaid and overworked. They rarely receive merit or cost of living raises. The facilities that desperately need them are having a very difficult time making ends meet. This is because Medicaid, which pays for nearly half of all LTC in the United States, pays nursing homes significantly less than the cost of care.

Nursing homes which accept Medicare for rehabilitation care (their main source of revenue) must also accept Medicaid—the welfare program which pays for care when the patient cannot afford it. Thus, the nursing home has become the main place that will accept a person if he/she cannot pay for care in an assisted living facility. Assisted living facilities cost between $4000 and $8000 a month depending on care needs. Since they do not receive Medicare for rehabilitation care, they are not required to accept Medicaid, and many do not.

Most people cannot afford the monthly charges for long without LTC insurance.

The problem is that many people do not plan for care in later life, with investments or insurance that pays for LTC. Many of the residents in LTC facilities are on Medicaid, and most of them are in nursing homes. This is because the very nice assisted living facilities are rapidly deciding not to accept Medicaid because of its inadequate reimbursement for care.

Back to the CNAs I met in the hospital. While there is a desperate need for caregivers, those caregivers need a living wage, and many long-term care facilities are unable to provide that. So, they migrate to the hospitals who can pay them and provide benefits.

If you want to have good long- term care, in a place that appeals to you when your health changes, you need to have a plan to pay for that care or the odds may be good that a nursing home may be your only choice. Years ago, I purchased LTC insurance that will pay for the care I need, in a setting I will be happy in when that time comes. Will you?

For more information, browse all of our resources at www.TheLongTermCareGuy.com.

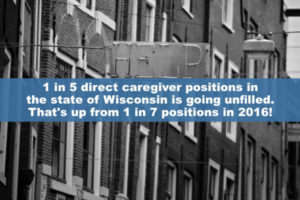

Wisconsin’s Long-Term Care Workforce At Crisis Level

A coalition of Wisconsin health care organizations is warning that the state’s shortage of long-term care providers in the workforce continues to grow!

by Brady Carlson, Wisconsin Public Radio

“A coalition of Wisconsin health care organizations is warning that the state’s shortage of long-term care providers continues to grow. The study, put together by several groups across the state, says 1 in 5 direct caregiver positions in the state is going unfilled. That’s up from 1 in 7 positions in 2016. Starting wages in the profession are so low that many potential workers never apply, according to the report. The median hourly starting wage for personal caregivers is $10.75 an hour, according to the study, while other positions outside health care start at $12 an hour. The report found Wisconsin’s low rate of Medicaid reimbursement is a key factor keeping provider wages low.”

Why can’t the assisted living facilities, the home care agencies, the nursing homes pay more and hire the people they need? The answer is because so many care recipients did not plan to be able to pay for this care and went broke – ending up on a welfare program called Medicaid. Medicaid pays far less than the cost of your care. Thus the care providers cannot pay more for employees and end up short handed.

Do you want to search for a place to care for you? Do you want to depend on government welfare to pay for this? Do you think the government can fund all the care needed by the baby boomers who are turning 65 at a rate of 10,000 per day which will increase in the next seven years to 12,500 per day? Do you also believe in Santa Claus and the Easter Bunny?

Or do you feel lucky today, perhaps you will never need care as you age (70% will per HHS). Personally I am hoping to be shot by a jealous husband at age 99, but I doubt that will happen. Thus I purchased LTC insurance way back when I was 52, in good health, and it was much less than if I waited until after 65.

I can now pay for whatever care I need. If I do not like the care I am getting, I can vote with my feet (or my wheelchair) and go to a place that can hire enough caregivers because I am paying what it costs for my care. I am pretty sure there will be others at the same facility, able to pay because they are extremely rich, or like I, they purchased LTC insurance.

What is your plan? If you don’t think you have a plan, you actually do – go broke and hope for the best on welfare (Medicaid). If you would like to investigate what plans can benefit you, contact the experts in LTC planning, not someone who dabbles, or also has a policy. Call www.TheLongTermCareGuy.com at 884-3030 and find out all the ways you can be taken care of, no matter your health or finances.

Get a FREE Estimate from The Long Term Care Guy!

Immigration Problem, or Caregiver Problem?

Immigrants make up 1 in 4 health aide workers.

From the Washington Post

BOSTON — After back-to-back, eight-hour shifts at a chiropractor’s office and a rehab center, Nirva arrived outside an elderly woman’s house just in time to help her up the front steps. Nirva took the woman’s arm as she hoisted herself up, one step at a time, taking breaks to ease the pain in her hip. At the top, they stopped for a hug.

The women each bear accents from their homelands: Nirva, who asked that her full name be withheld, fled here from Haiti after the 2010 earthquake. Dicenso moved here from Italy in 1949. Over the years, Nirva, 46, has helped her live independently, giving her showers, changing her clothes, washing her windows, taking her to her favorite parks and discount grocery stores. Now Dicenso and other people living with disabilities, serious illness and the frailty of old age are bracing to lose caregivers like Nirva due to changes in federal immigration policy.

Nirva is one of about 59,000 Haitians living in the U.S. under Temporary Protected Status (TPS), a humanitarian program that gave them permission to work and live here after the January 2010 earthquake devastated their country. Many work in health care, often in grueling, low-wage jobs as nursing assistants or home health aides.

Now these workers’ days are numbered: The Trump administration decided to end TPS for Haitians, giving them until July 22, 2019, to leave the country or face deportation.

In Boston, the city with the nation’s third-highest Haitian population, the decision has prompted panic from TPS holders and pleas from health care agencies that rely on their labor. The fallout offers a glimpse into how changes in immigration policy are affecting older Americans in communities around the country, especially in large cities.

Ending TPS for Haitians “will have a devastating impact on the ability of skilled nursing facilities to provide quality care to frail and disabled residents,” warned Tara Gregorio, president of the Massachusetts Senior Care Association, which represents 400 elder care facilities, in a letterpublished in The Boston Globe. Nursing facilities employ about 4,300 Haitians across the state, she said.

“We are very concerned about the threat of losing these dedicated, hardworking individuals, particularly at a time when we cannot afford to lose workers,” Gregorio said in a recent interview. In Massachusetts, 1 in 7 certified nursing assistant (CNA) positions are vacant, a shortage of 3,000 workers, she said.

Nationwide, 1 million immigrants work in direct care — as CNAs, personal care attendants or home health aides — according to the Paraprofessional Healthcare Institute, a New York-based organization that studies the workforce. Immigrants make up 1 in 4 workers, said Robert Espinoza, PHI’s vice president of policy. Turnover is high, he said, because the work is difficult and wages are low. The median wage for personal care attendants and home health aides is $10.66 per hour, and $12.78 per hour for CNAs. Workers often receive little training and leave when they find higher-paying jobs at retail counters or fast-food restaurants, he said.

The country faces a severe shortage in home health aides. With 10,000 baby boomers turning 65 each day, an even more serious shortfall lies ahead, according to Paul Osterman, a professor at Massachusetts Institute of Technology’s Sloan School of Management. He predicts a national shortfall of 151,000 direct care workers by 2030, a gap that will grow to 355,000 by 2040. That shortage will escalate if immigrant workers lose work permits, or if other industries raise wages and lure away direct care workers, he said.

Nursing homes in Massachusetts are already losing immigrant workers who have left the country in fear, in response to the White House’s public remarks and immigration proposals, Gregorio said. Nationally, thousands of Haitians have fled the U.S. for Canada, some risking their lives trekking across the border through desolate prairies, after learning that TPS would likely end.

Employers are fighting to hold on to their staff: Late last year, 32 Massachusetts health care providers and advocacy groups wrote to the Department of Homeland Security urging the acting secretary to extend TPS, protecting the state’s 4,724 Haitians with that special status.

“What people don’t seem to understand is that people from other countries really are the backbone of long-term care,” said Sister Jacquelyn McCarthy, CEO of Bethany Health Care Center in Framingham, Mass., which runs a nursing home with 170 patients. She has eight Haitian and Salvadoran workers with TPS, mostly certified nursing assistants. They show up reliably for 4:30 a.m. shifts and never call out sick, she said. Many of them have worked there for over five years. She said she already has six CNA vacancies and can’t afford to lose more. “There aren’t people to replace them if they should all be deported,” McCarthy said.

Who will care for you? How much will they be paid? When you cannot hire enough workers to fill the job, wages go up. Can you afford long-term care today? How about in 15 or 30 years when the costs have doubled or quadrupled? I can, due to the LTC insurance I bought years ago. Its benefits get larger every year by 5% compound to (just) keep up with increasing costs for care. If you don’t have yours yet, call (920) 884-3030 and talk to Romeo Raabe, TheLongTermCareGuy.com. Or look us up online first. Don’t wait until your health changes and you can no longer get this insurance.